ECONOMICS

This section on economics begins with a subject I found most important and interesting, mainly the distribution of income between wages and profits. This distribution, which has changed much for the worse since this article was published in 1981 in The Cambridge Journal of Economics, is a reflection of the balance or imbalance of power between countervailing powers in society. Since the election of 1980, the power of unions, the main countervailing power to our corporate plutocracy, has been weakened under Republicans and Democrats alike. The article linked to is an economic and statistical critique of a study by Thomas Weisskopf on the dependence of labor's share on "labor strength."

| wages_profits_share001.pdf |

The following op-ed piece focuses on a number of fallacious charges against the Social Security system, specifically the Trust Fund.

We don't have to destroy Social Security to save it

ROANOKE TIMES, April 16, 2011

Frank Munley

Munley taught physics and lives in Salem.

Suppose you go to a bank, get a loan of $100,000 and buy a house with it. A week later, the president of the bank sees you and says, "I hear we loaned you a hunk. How's our money?" And you say, "Like it or not, the money is gone -- I spent it." Outraged, the banker says. "Thanks for leaving us with an IOU!"

Now the foregoing scenario is nonsense. Bankers know very well that loans will be used to buy something -- almost always an investment in some real economic asset, like a house. You will repay it with future income, and if you fail to repay, the bank can take possession.

The "like it or not" statement above is just one of many politically loaded statements in Brian Lindholm's op-ed, "How to fix Social Security" (March 22).

Over the years, Social Security has loaned the government its sizable surplus, i.e., it has been one of the federal government's many bankers, along with China, pension and insurance funds, etc.

The government has used these borrowings much like private parties do: to invest in the future by spending on education, health, welfare, defense (too much for me), safety regulation, basic research and other things that make living in this country worthwhile.

Saying these government expenditures are not investments in real assets (as claimed by President Clinton's Office of Management) is to buy into the snake oil of right-wing ideologues whose regulation-hating, financial-instrument craziness (another Clinton legacy) led to the recent banking crisis, the ensuing "Great Repression" and huge jump in the national debt.

Sadly, President Obama has threatened Social Security with his cut in its payroll tax to be made up now by the tender mercies of the congressional budget process.

The recent shortfall of Social Security tax revenues is a short-term problem brought about by the recession/depression, which has left unemployment far above normal. This revenue crisis will be over when the economy straightens out, either by an upswing in the business cycle or sufficiently strong government stimulus.

And contrary to Lindholm's false fears, the U.S. government will honor all debts, foreign and domestic, assuming right-wing anarchists in Congress fail to freeze the debt ceiling.

There is a long-term problem for Social Security, but Lindholm ignores the simple and fair solution: Raise the ceiling on the payroll tax, currently set at $106,800, and adjust it for inflation to ensure the program's solvency for the foreseeable future.

There are sound economic reasons, ably expounded by former Labor Secretary Robert Reich, to extend the ceiling to $180,000 to compensate for the swing of national income to the wealthy. What a dubious distinction the U.S. has: The top 1 percent of income recipients rake in 21 percent of the income (up from about 12 percent in 1984), and average executive compensation is almost 400 times the average factory worker income, a ratio not even approached by other industrialized democracies.

Rectifying the maldistribution of income by eliminating the Bush tax cuts for the wealthy, imposing a truly progressive income tax, and reforming our corrupt electoral process to impose the political will of the people on Congress will ensure that the government can meet its debts without unnecessary inflation.

Lindholm offers the morally imperious argument that current recipients of Social Security are freeloading on younger wage earners (as if the young pulled themselves up by their bootstraps and owe nothing to those who labored lovingly to give us the living conditions we have), and says the Social Security retirement age (more accurately, the full benefit age) should be raised.

But not everyone has the health to continue working past 65, and anyway, raising the age is unnecessary if the ceiling on the payroll tax is raised.

Furthermore, with pension funds faltering, many young people will feel a responsibility to take care of elderly parents, and curtailing Social Security benefits will make it all the more difficult. I first paid Social Security tax more than 50 years ago with the understanding that I could retire at 65. Don't change the rules in the middle of the game.

Lindholm concludes, "Heaven knows I'd enjoy a lengthy 30-year retirement, but I cannot rightly demand that other people pay for it." A 30-year retirement is extremely rare -- someone retiring at 65 would have to live to 96, well beyond the average of 78. And why say without qualification "other people"? You can't get Social Security unless you pay into the fund, and what you get is determined by how much you put in.

ROANOKE TIMES, April 16, 2011

Frank Munley

Munley taught physics and lives in Salem.

Suppose you go to a bank, get a loan of $100,000 and buy a house with it. A week later, the president of the bank sees you and says, "I hear we loaned you a hunk. How's our money?" And you say, "Like it or not, the money is gone -- I spent it." Outraged, the banker says. "Thanks for leaving us with an IOU!"

Now the foregoing scenario is nonsense. Bankers know very well that loans will be used to buy something -- almost always an investment in some real economic asset, like a house. You will repay it with future income, and if you fail to repay, the bank can take possession.

The "like it or not" statement above is just one of many politically loaded statements in Brian Lindholm's op-ed, "How to fix Social Security" (March 22).

Over the years, Social Security has loaned the government its sizable surplus, i.e., it has been one of the federal government's many bankers, along with China, pension and insurance funds, etc.

The government has used these borrowings much like private parties do: to invest in the future by spending on education, health, welfare, defense (too much for me), safety regulation, basic research and other things that make living in this country worthwhile.

Saying these government expenditures are not investments in real assets (as claimed by President Clinton's Office of Management) is to buy into the snake oil of right-wing ideologues whose regulation-hating, financial-instrument craziness (another Clinton legacy) led to the recent banking crisis, the ensuing "Great Repression" and huge jump in the national debt.

Sadly, President Obama has threatened Social Security with his cut in its payroll tax to be made up now by the tender mercies of the congressional budget process.

The recent shortfall of Social Security tax revenues is a short-term problem brought about by the recession/depression, which has left unemployment far above normal. This revenue crisis will be over when the economy straightens out, either by an upswing in the business cycle or sufficiently strong government stimulus.

And contrary to Lindholm's false fears, the U.S. government will honor all debts, foreign and domestic, assuming right-wing anarchists in Congress fail to freeze the debt ceiling.

There is a long-term problem for Social Security, but Lindholm ignores the simple and fair solution: Raise the ceiling on the payroll tax, currently set at $106,800, and adjust it for inflation to ensure the program's solvency for the foreseeable future.

There are sound economic reasons, ably expounded by former Labor Secretary Robert Reich, to extend the ceiling to $180,000 to compensate for the swing of national income to the wealthy. What a dubious distinction the U.S. has: The top 1 percent of income recipients rake in 21 percent of the income (up from about 12 percent in 1984), and average executive compensation is almost 400 times the average factory worker income, a ratio not even approached by other industrialized democracies.

Rectifying the maldistribution of income by eliminating the Bush tax cuts for the wealthy, imposing a truly progressive income tax, and reforming our corrupt electoral process to impose the political will of the people on Congress will ensure that the government can meet its debts without unnecessary inflation.

Lindholm offers the morally imperious argument that current recipients of Social Security are freeloading on younger wage earners (as if the young pulled themselves up by their bootstraps and owe nothing to those who labored lovingly to give us the living conditions we have), and says the Social Security retirement age (more accurately, the full benefit age) should be raised.

But not everyone has the health to continue working past 65, and anyway, raising the age is unnecessary if the ceiling on the payroll tax is raised.

Furthermore, with pension funds faltering, many young people will feel a responsibility to take care of elderly parents, and curtailing Social Security benefits will make it all the more difficult. I first paid Social Security tax more than 50 years ago with the understanding that I could retire at 65. Don't change the rules in the middle of the game.

Lindholm concludes, "Heaven knows I'd enjoy a lengthy 30-year retirement, but I cannot rightly demand that other people pay for it." A 30-year retirement is extremely rare -- someone retiring at 65 would have to live to 96, well beyond the average of 78. And why say without qualification "other people"? You can't get Social Security unless you pay into the fund, and what you get is determined by how much you put in.

HOW MUCH DO YOU PUT IN AND HOW MUCH DO YOU GET OUT OF SOCIAL SECURITY?

The following was a preface to an e-mail message I sent to colleagues containing the foregoing article on Social Security. It refers to the fiscal and debt situation in April 2016.

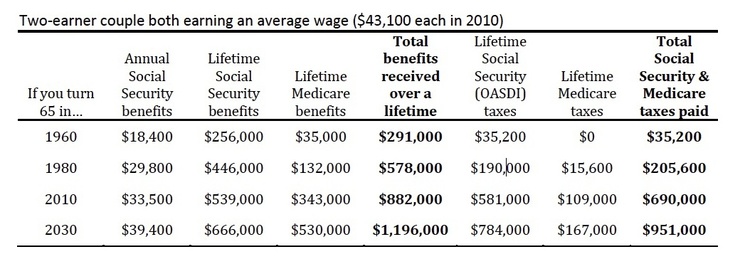

Let's look at who pays for what Social Security recipients get from the system. The following interesting table shows how much a typical couple put into SS and how much they take out (assuming average life span). It's from the Urban Institute (you can access other tables at http://www.urban.org/publications/412281.html ):

As the table shows, "Lifetime SS benefits" (column 3) for a couple turning 65 last year is smaller than "Lifetime SS (OASDI) taxes" (column 6). This puts the lie to the claim that SS beneficiaries are in some way stealing from current taxpayers, which is not to ignore the fact that right now there are only 4.6 people of working age for every person beyond the retirement age, and this number is expected to decrease. (See The Economist, 9 April 2011 Special Section on pensions for more information.) I'm not sure why column 3 is so much larger than column 6 in previous years. I know the ceiling on SS taxes was raised in the mid-80s which might explain it. I'll contact the authors of the report and get back to you on it. As I say below, another increase is very much in order! (In my opinion, there should be no ceiling--all for one, one for all.)

The next big crisis issue confronted in Spring, 2011 was the debt ceiling. Let's see if know-nothing congressional anarchists (like Ayn Rand acolyte Paul Ryan and his star-struck followers) are stupid enough not to raise the debt ceiling. After that, we have Medicare and Medicaid to worry about--much tougher issues than SS, as suggested by the above table. But we are not a poor country! The national security apparatus (aka the military-industrial complex) could be cut by 50% and the freed-up tax revenues could easily help Medicare survive as is. Of course, it hasn't helped that Obama's half-pregnant health care plan does precious little to control health care costs. Control would require a strong public-option plan, which Obama pretended to want but didn't. (Single payer--i.e., "Medicare for All" as proposed by then-House Speaker Nancy Pelosi--would have been even better.)

As MSNBC's Ed Schultz said last night on the Bill Maher show, we ought to get some things like Medicare and SS OFF the table in budget negotiations. Let's start an "OFF THE TABLE" movement!